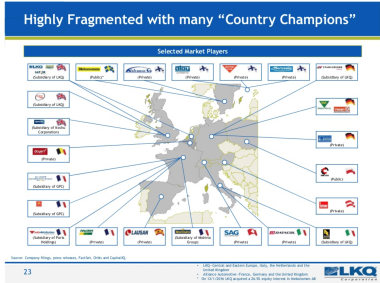

Three market players that capture 60% of European business in order to endure and export; OEMs sized to cope with the pressure from these distribution giants and stay competitive in their speciality, investment in R&D for the future. All these challenges are an indication that the market concentration currently underway is not likely to slow down on either side of the IAM. “There will be no end to mergers and acquisitions until monopolistic considerations come to bear”, warns Fotios Katsardis (Temot). In the West, the distribution picture is already clear: Benelux, Denmark, Germany and the UK are concentrated. However there remain significant opportunities in France, Italy, Spain and Poland. The East is becoming the new playground. “Many distributors are looking to sell their business. Because after 25 years of working on a demand-driven market, they are required to start selling, which is an entirely different proposition”, describes Hans Eisner (GAUI). If these personalities are to be believed, this wave of concentration is beneficial to the independent aftermarket. Nowadays, European management teams talk among themselves, with each feeling that they benefit: higher margins for some, volume and market share gained for others.

The little ones worriedBut this ideal world is perceived by smaller firms as a loss of freedom to act. The number of approved suppliers listed by the “big three” is being cut back, while the others expand their brand portfolio. “We can already see distortion occurring in terms of margins, as not all suppliers can withstand the pressure applied by multinational clients and which will tend to further widen the gap between the multinational and the traditional medium-sized family-owned company.” Second tier suppliers are also in a difficult position, since they are subject to pressure from their upmarket competitors and from suppliers from Asia, which are particularly aggressive through their economic quality and constant improvement. There will be further casualties.Caroline Ridet